IN THIS SECTION

CFPB Report: 2014-AE-C-005 March 27, 2014

The CFPB Can Improve the Efficiency and Effectiveness of Its Supervisory Activities

available formats

-

Executive Summary:

PDF | HTML -

Full Report:

PDF (2 MB) | HTML

Introduction

Objectives

The Office of Inspector General (OIG) conducted an evaluation of the Consumer Financial Protection Bureau’s (CFPB) supervision program. Our objectives for this evaluation included (1) reviewing key program elements, such as policies and procedures, examination guidance, and controls to promote consistent and timely reporting; (2) assessing the approach for staffing examinations; and (3) assessing the training program for examination staff. This evaluation was our initial opportunity to assess the operational efficiency and effectiveness of the CFPB’s supervisory program; therefore, we chose to focus on the foundational components of the program.

To fulfill our objectives, we reviewed the CFPB’s practices for scheduling, staffing, and conducting examinations, including any coordination with the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, the National Credit Union Administration, and the Office of the Comptroller of the Currency (hereafter, the prudential regulators). We also assessed the examination report drafting and review process as well as the CFPB’s processes for monitoring its performance against the agency’s expectations for timely reporting. Finally, we analyzed the CFPB’s training program for examination staff, including the development of the agency’s examiner commissioning program. We describe our scope and methodology in greater detail in appendix A.

Background

The Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) established the CFPB to regulate the offering and provision of consumer financial products and services under the federal consumer financial laws. To carry out this mission, the Dodd-Frank Act granted the CFPB authority to supervise the following types of consumer financial market participants:

- insured depository institutions, credit unions, and their affiliates, with more than $10 billion in total assets1

- certain nondepository institutions, including entities in the consumer mortgage, private-education lending, and payday lending markets; larger participants in markets for other consumer financial products or services as defined by the CFPB; and entities the CFPB has reasonable cause to determine, by order, are “engaging, or ha[ve] engaged, in conduct that poses risks to consumers with regard to the offering or provision of consumer financial products or services”2

In July 2011, the CFPB commenced operations and initiated its supervision program for depository institutions with more than $10 billion in total assets. By law, the CFPB could not exercise its authority to supervise nondepository institutions until the appointment of its Director. On January 4, 2012, the President appointed Richard Cordray as the Director of the CFPB, and the following day, the CFPB announced the launch of its supervision program for nondepository institutions.3

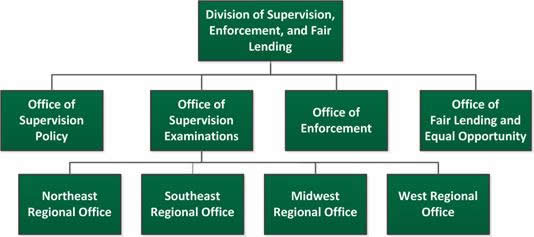

The CFPB’s Division of Supervision, Enforcement, and Fair Lending (SEFL) conducts the agency’s supervision activities. The agency originally organized its supervision activities according to its dual responsibility to supervise depository and nondepository institutions. However, in December 2012, the CFPB announced that it had reorganized its supervision structure to enhance its effectiveness and efficiency. As a result of this reorganization, the CFPB established within SEFL the Office of Supervision Examinations and the Office of Supervision Policy. Both offices address depository and nondepository institution supervision. Figure 1 illustrates SEFL’s organizational structure.

Figure 1: SEFL Organizational Structure

Source: OIG compilation based on a review of CFPB organizational charts.

Note: This organizational chart is not comprehensive and includes detail relevant to this evaluation.

The Office of Supervision Examinations oversees the CFPB’s examination efforts and seeks to ensure that policies and procedures are followed. This office also manages the recruiting, training, and commissioning processes for CFPB examiners. The agency’s four regional offices, located in New York (Northeast), Washington, DC (Southeast), Chicago (Midwest), and San Francisco (West), report to the Office of Supervision Examinations. As of December 12, 2013, the CFPB had 319 examiners employed at its four regional offices.

The Office of Supervision Policy seeks to ensure that supervision decisions are consistent with applicable laws and the CFPB’s mission. It also is responsible for ensuring that supervision decisions are consistent across markets, charters, and regions.

In addition to the two supervision offices, SEFL includes the Office of Enforcement4 and the Office of Fair Lending and Equal Opportunity.5 These offices work in close coordination with the supervision offices.

Coordination With the Prudential Regulators

The Dodd-Frank Act requires the CFPB to coordinate certain supervisory activities with the prudential regulators to minimize regulatory burden. To address this requirement, the CFPB and the prudential regulators signed a memorandum of understanding (MOU) that includes guidance on how the agencies must coordinate examination scheduling and share draft reports of examination for institutions supervised by the CFPB and another prudential regulator.

According to the MOU, the CFPB and the prudential regulators will “generally” execute examinations of depository institutions simultaneously, subject to certain exceptions. Notably, the MOU states that examinations are simultaneous if “material portions” of each agency’s examinations are conducted during a concurrent time period. Further, the institution may request that the CFPB and the prudential regulator conduct their examinations separately.

The MOU also addresses the Dodd-Frank Act requirement that the agencies “share each draft report of examination with the other agency and permit the receiving agency a reasonable opportunity (which shall not be less than a period of 30 days after the date of receipt) to comment on the draft report before such report is made final.” According to the MOU, the agencies are required to share only reports of examination prior to issuance, not supervisory letters.

Types of Supervisory Examinations, Products, and Actions

In general, the CFPB conducts the following types of examinations: (1) limited-scope examinations, which target a product line, a regulation, or an institution’s compliance management system, or (2) full-scope examinations, which include an evaluation of an institution’s compliance management system and summarize the significant conclusions about the product lines reviewed, or of various limited-scope examinations. The CFPB may place certain institutions under a continuous supervision program whereby institutions have CFPB examiners present on a full-time basis. The examiners conduct a series of limited-scope examinations.

Depending on the type of examination, the agency will issue either (1) a report of examination, which details findings and communicates a rating to the supervised institution, or (2) a supervisory letter, which details findings but typically does not communicate a rating to the supervised institution. Generally, full-scope examinations result in an examination report, and limited-scope examinations result in a supervisory letter. In addition to supervisory letters and examination reports, the CFPB also conducts some examinations that do not result in written products, such as baseline reviews. The CFPB performs these baseline reviews to serve as the agency’s initial introduction to an institution’s compliance management system. Table 1 describes the products that the CFPB issues as a result of each type of examination.

Table 1: CFPB Examination Review Types and Products

| Type of review | Report of examination issued? | Supervisory letter issued? | Rating assigned? |

|---|---|---|---|

| Full-scope, continuous | Yes, the CFPB plans to issue reports at the end of an examination cycle, typically every 12–18 months | No | Yes, through a report of examination |

|

Full-scope, not continuous |

Yes, following the conclusion of the examination | No | Yes, through a report of examination |

| Baseline review | No | No | No |

| Limited-scope, continuous | No | Yes, following the conclusion of the review | No, unless a significant finding warrants a downgrade |

|

Limited-scope, not continuous |

No | Yesa | No, unless a significant finding warrants a downgrade |

Source: OIG summary of CFPB documentation.

aMay also result in a letter to the top-tier entity describing work conducted at an affiliated depository institution, a nondepository institution, or both.

Depending on the examination findings, some examinations may lead to nonpublic supervisory actions or public enforcement actions, which are civil actions brought against parties under the CFPB’s enforcement authorities. Nonpublic supervisory actions range in severity from recommendations, which serve as suggestions to the institution, to matters requiring attention, which require a response to the CFPB and include required time frames for resolution. The agency has issued several nonpublic supervisory actions. According to the March 2013 Semi-Annual Report of the Consumer Financial Protection Bureau,6 the agency issued a total of nine public enforcement actions during 2012, three of which resulted from examination findings.

Supervisory Activities

In executing its supervision authority, the CFPB focuses on an institution’s ability to detect, prevent, and correct practices that present a significant risk of violating federal consumer financial law. The CFPB’s supervision activities include (1) prioritizing and scheduling examinations, (2) planning and executing examinations, and (3) reporting findings in the form of reports of examination or supervisory letters.

Prioritizing and Scheduling Examinations

For the purpose of prioritizing its supervisory activities, the CFPB has identified various product lines offered to consumers by supervised institutions. For example, the CFPB refers to mortgages offered by “Institution A” and deposit products provided by “Institution B” as institution product lines. The Office of Supervision Examinations prioritizes 120–160 institution product lines to be examined each year based on an assessment of the risk for potential harm to consumers. The potential risk to consumers may vary significantly across institution product lines. As a result, an institution that originates mortgages and offers debit cards to consumers may undergo an examination of only one institution product line in any given year, depending on the results of the CFPB’s risk assessment.

Once the CFPB prioritizes institution product lines, its regional management is responsible for scheduling examinations. In addition to risk of harm to consumers, regional managers also consider other factors when scheduling examinations, such as availability of staff resources and the Dodd-Frank Act requirement to coordinate examination scheduling. Each region is responsible for scheduling and staffing its examinations, and managers have discretion in the method they use for scheduling an examination team.

Planning and Executing Examinations

An examination team, led by an examiner in charge, is responsible for planning and conducting each examination. The examination team begins the examination process by contacting the supervised institution and gathering available information on the relevant institution product line from a variety of external sources and sources within the agency. Based on a review of that information and discussions with other CFPB staff, the examination team defines the examination scope and communicates the agency’s anticipated supervisory activities to the supervised institution during an entrance meeting.

The examination team then initiates fieldwork by conducting examination procedures. This work typically involves gathering and analyzing data at the institution. The CFPB Supervision and Examination Manual (examination manual) describes examination procedures based on the product line being examined as well as the applicable federal law or regulation.7 The examination manual also contains a broad overview of the examination process and the examination rating definitions established by the Federal Financial Institutions Examination Council (FFIEC)8 and adopted by the CFPB.

Reporting Results of Examinations

In June 2012, the CFPB issued an internal policy, CFPB Process for Reviewing Supervisory Letters, Examination Reports, and Supervisory Actions (examination reporting policy), which provides (1) guidance on reviewing supervisory products and (2) timeliness requirements for the major examination reporting milestones. At the conclusion of the fieldwork phase, the examination team drafts a supervisory letter or report of examination summarizing its findings. The primary purpose of the letter or report is to communicate examination findings in their final form to the board of directors, principals, and senior executives of a supervised entity. After the draft is approved at the regional level, it is submitted to CFPB headquarters, where the Office of Supervision Policy provides input and circulates the draft to various stakeholders within headquarters, including the Office of Supervision Examinations, the Office of Enforcement, and the Office of Fair Lending and Equal Opportunity.

Once headquarters approves the draft, the region prepares the draft for issuance or transmittal to the relevant prudential regulator for comment. If the examination results in a supervisory letter or pertains to a nondepository institution, the CFPB may then issue the report. For examinations of depository institutions, the Dodd-Frank Act requires the CFPB to share draft reports of examination with the institution’s prudential regulator and allow the prudential regulator at least 30 days to submit any comments about the draft to the CFPB. Once the CFPB receives those comments and considers the suggestions, the agency may then issue the final report.

The CFPB has established timeliness requirements for certain milestones in the reporting phase. Table 2 summarizes the reporting milestones and the corresponding timeliness requirements established by the CFPB for examination reports and supervisory letters.

Table 2: CFPB Examination Reporting Timeliness Requirements

| Milestone |

Requirement (calendar days) |

|---|---|

| Regions provide draft to headquarters | 30 |

| Headquarters approves | 30 |

| Regions finalize the draft | 5 |

| Total time to issue final reports of examination for nondepository institutions and all supervisory letters | 65 |

| Prudential regulator comment period, if necessary | 30 |

| CFPB considers prudential regulator comments, if necessary | 15 |

| Total time to issue final reports of examination for depository institutions | 110 |

Source: CFPB Process for Reviewing Supervisory Letters, Examination Reports, and Supervisory Actions.

The CFPB uses a database called the Supervisory Examination System (SES) to monitor and track its progress toward issuing examination reports. SES serves as the system of record for CFPB examinations and includes information on the supervised institution, assigned staff, and the examination itself. The CFPB has made incremental upgrades to SES and is in the early stages of planning a comprehensive update to the system.

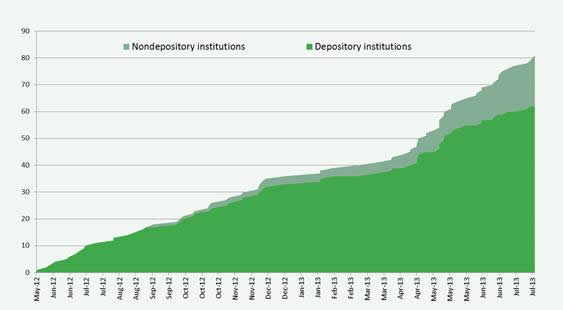

As of July 31, 2013, the CFPB issued 82 products resulting from completed examinations,9 including 35 reports of examination and 47 supervisory letters. Among those 82 examinations, 63 pertained to depository institutions and 19 pertained to nondepository institutions. Figure 2 illustrates the number of examination products issued by the CFPB according to the type of institution.

Figure 2: Cumulative Examination Products issued, May 2012 to July 2013

Source: OIG analysis of CFPB SES data.

Training Examination Staff

Currently, the CFPB is creating training courses and a commissioning program for examination staff. According to the CFPB, the examiner commissioning program will include a series of classes covering the knowledge and skills necessary to successfully conduct examinations, as well as on-the-job training. It will also require a written, validated test designed to evaluate a noncommissioned examiner’s readiness for the duties of a commissioned examiner.

- 1. Primary consumer protection supervisory authority for depository institutions with total assets of $10 billion or less was retained by those institutions’ prudential regulators. However, the Dodd-Frank Act granted the CFPB authority to participate in examinations of these smaller depository institutions on a sampling basis. Return to text

- 2. Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. No. 111-203, § 1024(a)(C), 124 Stat. 1376, 1987 (2010) (codified at 12 U.S.C. § 5514(a)(C) (2010)). Return to text

- 3. The President appointed the Director during a Senate recess, and on July 16, 2013, the Senate confirmed Richard Cordray as Director of the CFPB. Return to text

- 4. The Office of Enforcement is primarily responsible for initiating investigations and enforcement actions, when appropriate, to ensure that providers of consumer financial products and services comply with applicable laws and regulations. Return to text

- 5. The Office of Fair Lending and Equal Opportunity is primarily responsible for providing oversight and enforcement of fair lending laws to ensure that credit decisions are not based on race or any other prohibited factor. Return to text

- 6. Consumer Financial Protection Bureau, Semi-Annual Report of the Consumer Financial Protection Bureau, March 2013, http://files.consumerfinance.gov/f/201303_CFPB_SemiAnnualReport_March2013.pdf. Return to text

- 7. The CFPB Supervision and Examination Manual, version 2, was issued in October 2012 and is available at http://www.consumerfinance.gov/guidance/supervision/manual. Return to text

- 8. The FFIEC is a formal interagency body empowered to prescribe uniform principles, standards, and report forms for the federal examination of financial institutions by the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, the National Credit Union Administration, the Office of the Comptroller of the Currency, and the CFPB and to make recommendations to promote uniformity in the supervision of financial institutions. The FFIEC rating definitions uniformly rate institutions’ compliance programs from 1 (strong) to 5 (in need of strongest supervisory attention). Return to text

- 9. Completed examinations exclude baseline reviews, which are initial reviews of institutions’ compliance management programs that did not result in reports of examination or supervisory letters. Return to text