IN THIS SECTION

CFPB Report: 2014-AE-C-005 March 27, 2014

The CFPB Can Improve the Efficiency and Effectiveness of Its Supervisory Activities

available formats

-

Executive Summary:

PDF | HTML -

Full Report:

PDF (2 MB) | HTML

Finding 1: The CFPB Did Not Meet Reporting Timeliness Requirements

Our testing results indicate that the CFPB did not issue its examination reports consistently with the time frames established in its examination reporting policy. After fieldwork is completed, the requirements in the CFPB Process for Reviewing Supervisory Letters, Examination Reports, and Supervisory Actions allow 30 days for regions to submit a draft examination report to headquarters and 30 days for headquarters to approve that draft; the CFPB then has 5 days to either share the draft with the prudential regulator or issue a final product. According to CFPB officials, the agency has not met these requirements due to many factors, including the novel nature of several substantive issues raised during examinations and the “aspirational” nature of the agency’s timeliness requirements for examination reporting. Further, according to a senior official, in the early stages of implementing the CFPB’s supervision program, the agency focused on assuring consistent results as part of its examination report review process rather than timeliness. The CFPB’s inability to meet its timeliness requirements contributed to a considerable number of examination reports that have yet to be issued. These delays do not afford supervised institutions certainty concerning the CFPB’s feedback on the effectiveness of the institutions’ compliance programs or processes. Further, prolonged delays in issuing examination reports may expose the CFPB to reputational risk.

The CFPB Did Not Meet Internal Timeliness Requirements for Examination Reporting

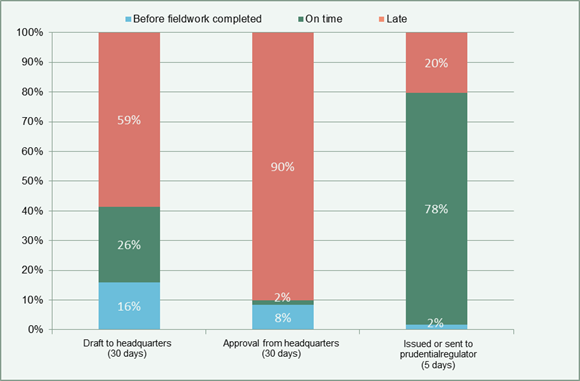

We found that 59 percent of the 82 drafts submitted by regional examination teams to CFPB headquarters during the scope of our evaluation did not meet the CFPB’s timeliness requirement for submission within 30 days of fieldwork completion. Moreover, 54 of the 60 drafts that received headquarters approval as of July 31, 2013, had not been approved by headquarters within the 30-day requirement. Once a draft received headquarters’ approval, the CFPB generally met its final reporting requirement for issuing a final product or sharing it with the prudential regulators. We found that the CFPB issued or shared approximately 78 percent of examinations within 5 days.10 Our analysis used SES data as of July 31, 2013, and included only those examinations for which fieldwork had been completed after June 15, 2012, when the agency issued the examination reporting policy. Figure 3 illustrates the CFPB’s reporting timeliness against the agency’s requirements.

Figure 3: CFPB Reporting Timeliness by Milestone

Source: OIG analysis of CFPB SES data.

Notes: Analysis includes only examinations with fieldwork completed after the CFPB issued its reporting requirements on June 15, 2012, through July 31, 2013. “Before fieldwork completed” reflects reporting milestones that were reached before the date fieldwork was completed, according to SES data. Percentages may not add to 100 due to rounding.

According to CFPB officials, the agency missed its timeliness requirements for various reasons. First, senior CFPB officials noted that the agency encountered several novel substantive examination issues, particularly those that arose during the initial federal examinations of nondepository institutions. The agency explained that such matters take longer to resolve because they involve complex issues that are highly dependent on the relevant facts and circumstances. Agency officials indicated that they have been deliberate in resolving those issues due to the precedent-setting nature of its decisionmaking and the need for consistent results. Second, the agency’s examination processes are still being refined. Third, one senior official said that in the early stages of implementing its supervision program, the agency focused on assuring consistent results as part of its examination report review process to the detriment of timeliness. Officials said that as the agency’s processes mature, the CFPB intends to streamline the review process to improve the timeliness of examination reporting while maintaining consistency in its examination products.11 Finally, several senior officials said that the timeliness requirements outlined in the examination reporting policy mentioned above were “aspirational,” and two agency officials opined that the reporting time frames are unrealistic. As a result, the CFPB does not actively monitor its performance against these timeliness requirements.

Reporting Delays Contributed to a Significant Number of Examination Reports That Have Not Been Issued

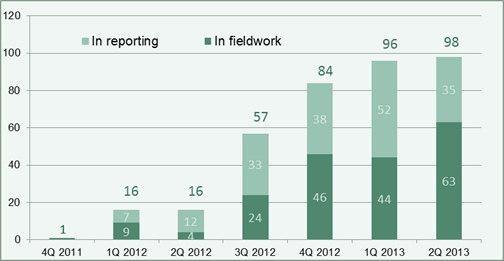

The CFPB’s reporting delays have contributed to a significant number of outstanding examinations. Although the CFPB has not monitored its performance against reporting requirements, it does track the number of examinations outstanding for longer than 90 days from the scope start date, including those in fieldwork and reporting.12 Several of these examinations have been outstanding for more than a year, indicating that the agency is not providing timely written feedback to the institutions it supervises. As previously mentioned, the primary purpose of the supervisory letter or report of examination is to communicate examination findings in their final form to the supervised entity. Absent timely written feedback in final form, institutions may not take action to correct potential issues with the consumer financial products and services they provide. Industry groups and other stakeholders have raised concerns about the length of the examination process, citing the uncertainty it creates for supervised institutions. Figure 4 illustrates the number of CFPB examinations outstanding for longer than 90 days.

Figure 4: CFPB Examinations Outstanding Longer Than 90 Days from Scope Start Date, Fourth Quarter 2011 to Second Quarter 2013

Source: OIG analysis of CFPB SES data.

As shown in figure 4, the number of examinations outstanding for longer than 90 days grew steadily from one examination at the end of 2011 to 98 examinations by the second quarter of 2013. Examinations in the reporting phase increased from 7 in the first quarter of 2012 to 52 by the first quarter of 2013, before dropping to 35 the following quarter. An increase in the number of examinations in the fieldwork phase, from 44 to 63 examinations during this same period, more than offset the decrease in examinations in reporting.

According to CFPB officials, the agency focused on reducing the number of examinations outstanding for longer than 90 days by addressing the specific causes of the delays. However, the CFPB does not have a formally documented and approved plan that identifies when and how these examinations will be reduced to a manageable level. Senior supervision officials meet weekly to discuss all examinations with a focus on clearing those that have been outstanding the longest. A senior official indicated that through this effort, the CFPB seeks to reduce the population of examinations by approximately 15 to 20 per month until the agency has 30 outstanding at any given time, but the senior official did not commit to a time frame for reaching that target. The CFPB continues to initiate new examinations while it works to reduce the number of examinations outstanding for longer than 90 days.

Management Actions Taken

Our fieldwork concluded in October 2013, and our evaluation used data as of July 2013. According to the CFPB, since that time, senior officials have expended considerable effort to clear the examination reports that have not been issued, contributing to a recent reduction in the number of outstanding examinations. In addition, in December 2013, the agency revised its methodology for measuring the number of outstanding examinations to exclude any examinations in the fieldwork phase, which also contributed to the reduction. Further, the CFPB has hired a consulting firm to assess its report review process to identify possible process enhancements and improve timeliness. Senior officials have indicated that the agency has piloted new approaches designed to streamline the reporting process, including identifying lower-risk products that may be issued by the regions without further review by headquarters staff. We intend to conduct future follow-up activities to determine whether the CFPB’s actions are responsive to the concerns raised in this finding.

Summary

The CFPB has not met its internal timeliness requirements for submitting drafts to headquarters or for receiving headquarters’ approval. Nearly 60 percent of the drafts submitted by regional examination teams to CFPB headquarters and 90 percent of the drafts that received headquarters approval did not meet the agency’s timeliness requirements. Delays in the reporting process have contributed to a significant number of examinations outstanding for longer than 90 days, which the agency had not developed specific targets to address during the scope of our review. The CFPB’s inability to provide examination reports to institutions in a timely manner creates uncertainty for supervised institutions. According to a senior official, concerted efforts to clear delayed examinations have led to a reduction in outstanding examinations after the completion of our fieldwork. In addition, the agency has piloted new approaches designed to streamline the reporting process.

Recommendations

We recommend that the Associate Director for SEFL

- Monitor the timeliness of examination reporting against the requirements the agency established in June 2012 and work to resolve any issues that cause reporting delays.

- Develop and document a formal plan with specific targets to reduce the number of examination reports yet to be issued to a manageable level, as defined in the formal plan.

Management's Response

Regarding recommendation 1, the Deputy Director and Associate Director for SEFL stated the following:

We will include a new metric in the regular reports currently provided to senior management regarding examination timeliness that specifically measures the status of report drafts against the internal requirements established by applicable CFPB policies. While the necessary information to determine examination timeliness is already in the reports, we agree that including a more salient measurement against the self-imposed policy requirements would be helpful.

We appreciate the Report’s acknowledgement of the extensive efforts currently underway at the CFPB to increase the effectiveness and efficiency of CFPB report preparation and review processes, including our efforts to address the numerous novel issues that often arise in CFPB examinations without sacrificing consistency across regions and types of institutions. These efforts have resulted in a substantial reduction since July 2013 in the number of outstanding CFPB examination reports.

As part of these overall efforts, the CFPB will be reevaluating its earlier June 2012 policy and the internal requirements established in that policy. Any new reporting metrics adopted will conform with the requirements established in any revised policies and procedures.

Regarding recommendation 2, the Deputy Director and Associate Director for SEFL stated the following:

As discussed in the Report, CFPB senior management is focused on maintaining an effective, efficient, and consistent supervision and examination process. The Report recognizes several of the various initiatives the CFPB has undertaken as we have continued to improve the timeliness of our report issuance process. We agree that adoption of a formal plan would be an effective tool in connection with these efforts, and would help memorialize many of the steps the CFPB has already taken. We will incorporate such a plan into our existing report review processes.

Management’s full response is included as appendix B.

OIG Comment

In our opinion, the actions described by the Deputy Director and Associate Director for SEFL appear to be responsive to our recommendations. We plan to follow up on the CFPB’s actions to ensure that each recommendation is fully addressed.

- 10. We did not evaluate the timeliness requirements associated with the CFPB receiving and considering comments to drafts from the prudential regulators, as these requirements only pertained to a subset of the total draft reports and these steps in the process are subject to factors beyond the CFPB’s control. Return to text

- 11. We understand that the CFPB has hired a consultant to assess the agency’s reporting process. Return to text

- 12. The CFPB also includes baseline compliance management reviews, which do not result in reports of examination or supervisory letters, in its monitoring of outstanding examinations. As of the second quarter of 2013, 14 of the 98 outstanding examinations were baseline compliance management reviews. Return to text