IN THIS SECTION

CFPB Report: 2013-AE-C-021 December 16, 2013

The CFPB Should Reassess Its Approach to Integrating Enforcement Attorneys Into Examinations and Enhance Associated Safeguards

available formats

-

Executive Summary:

PDF | HTML -

Full Report:

PDF (3 MB) | HTML - Accessible version

Introduction

Objectives

In the fall of 2012, the Office of Inspector General Hotline received a complaint regarding the activities of Consumer Financial Protection Bureau (CFPB) enforcement attorneys during an examination. In response, we reviewed materials submitted by the complainant and conducted interviews with members of that examination team, including those responsible for supervising the examination. Subsequently, we decided to initiate a broader evaluation of the CFPB's integration of enforcement attorneys into its examinations of depository and nondepository institutions' compliance with applicable federal consumer financial laws and regulations. Our objectives for the evaluation were to assess (1) the potential risks associated with this approach to conducting examinations and (2) the effectiveness of any safeguards that the CFPB adopted to mitigate the potential risks associated with this examination approach.1 For additional information regarding our scope and methodology, see appendix A.

Background

Federal Regulatory Structure for Overseeing Consumer Financial Protection Matters

The Board of Governors of the Federal Reserve System (Federal Reserve Board), the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency, collectively referred to herein as the federal banking agencies, each have a dual role in supervising certain entities within their jurisdictions to ensure their (1) safety and soundness and (2) compliance with applicable federal consumer financial laws2 and regulations. The Federal Reserve Board oversees state-chartered banks that are members of the Federal Reserve System,3 the Federal Deposit Insurance Corporation oversees state-chartered banks that are not members of this system, and the Office of the Comptroller of the Currency supervises national banks.

In addition to the federal banking agencies described above, the Federal Trade Commission (FTC) has certain authorities for enforcing applicable consumer protection laws and regulations. These authorities apply to nondepository institutions; however, the FTC does not have the authority to regularly examine such institutions in order to assess their compliance with those laws and regulations.4

Prior to the passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) and the subsequent transfer of certain authorities to the CFPB one year later, these federal regulators predominantly shared supervision and enforcement authorities over entities that provide consumer financial products and services. Critics of this regulatory structure often opined that it was fragmented. Moreover, some suggested that the federal banking agencies' supervisory approach placed more emphasis on ensuring the safety and soundness of supervised institutions than on consumer financial protection. Critics argued that federal consumer financial regulatory authorities should be consolidated in a single regulator exclusively focused on consumer protection.5

On July 21, 2010, the Dodd-Frank Act was enacted, and title X of the statute established the CFPB to "regulate the offering and provision of consumer financial products or services under the Federal consumer financial laws."6 While the federal banking agencies and the FTC continue to have some consumer protection authorities, the Dodd-Frank Act provided the CFPB with several significant authorities in this area, as described below.

The CFPB's Authorities Regarding Supervision and Enforcement and Its Initial Implementation of These Activities

The Dodd-Frank Act provided the CFPB with the authority to supervise the following types of consumer financial market participants:

-

-

depository institutions with more than $10 billion in total assets7

- certain nondepository institutions, including entities in the consumer mortgage, private education lending, and payday lending markets; larger participants in markets for other consumer financial products or services as defined by the CFPB; and entities that the CFPB has reasonable cause to believe are "engaging, or ha[ve] engaged, in conduct that poses risks to consumers with regard to the offering or provision of consumer financial products or services"8

-

depository institutions with more than $10 billion in total assets7

In July 2011, the CFPB commenced its operations and also initiated its supervision program for large depository institutions. By law, the CFPB could not exercise its authority to regulate nondepository institutions until its director was appointed. On January 4, 2012, the President appointed the Director of the CFPB during a Senate recess.9 The following day, the CFPB announced that it had launched its supervision program for nondepository institutions.

The Dodd-Frank Act also provided the CFPB with the authority to take appropriate enforcement action to address violations of federal consumer financial laws. However, the CFPB does not have criminal enforcement authority. During the course of examinations, if CFPB examiners identify significant issues or potential violations of law, enforcement attorneys and their supervision colleagues in the CFPB's Division of Supervision, Enforcement, and Fair Lending (SEFL) collectively may initiate enforcement actions. In addition, pursuant to investigative activities, the agency may issue subpoenas for witness testimony or documentary evidence in relation to CFPB hearings or may issue civil investigative demands to entities that may have materials relevant to an investigation. According to the Dodd-Frank Act, the agency shall have the jurisdiction to grant "any appropriate legal or equitable relief with respect to a violation of Federal consumer financial law," including but not limited to civil monetary penalties, restitution, limitations on the activities or functions of the party against whom the action is brought, and public notification regarding the violation.10 The CFPB issued nine public enforcement actions according to the agency's March 2013 semiannual report.11

The CFPB's Supervision, Enforcement, and Fair Lending Organizational Structure

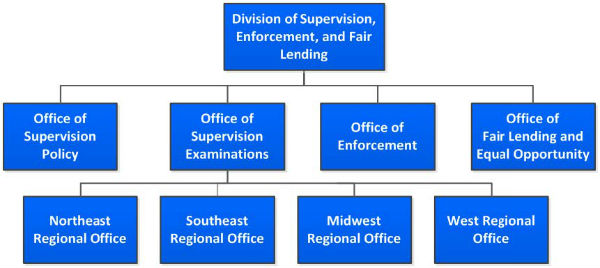

In April 2013, the CFPB published its five-year strategic plan.12 The plan defined the agency's mission as helping "consumer finance markets work by making rules more effective, by consistently and fairly enforcing those rules, and by empowering consumers to take more control over their economic lives." SEFL is a division within the CFPB that conducts activities that are central to the agency's consumer financial protection mission. The division has responsibility for conducting examinations of institutions' compliance with federal consumer financial protection laws and regulations, initiating enforcement actions when appropriate, and providing oversight and enforcement of fair lending laws.

The CFPB originally organized its supervision activities according to its dual responsibility to supervise depository and nondepository institutions. In December 2012, however, the CFPB announced that it had reorganized its supervision activities to enhance their effectiveness and efficiency. As a result of this reorganization, the CFPB established within SEFL the Office of Supervision Examinations and the Office of Supervision Policy, among other offices. Both offices address depository and nondepository institution supervision.

The Office of Supervision Examinations oversees the CFPB's examination efforts and works to ensure that policies and procedures are followed. This office also manages the recruiting, training, and commissioning processes for CFPB examiners. The Office of Supervision Examinations has four regional offices, located in New York (Northeast Regional Office), Washington, DC (Southeast Regional Office), Chicago (Midwest Regional Office), and San Francisco (West Regional Office).

The Office of Supervision Policy seeks to ensure that supervision decisions are consistent with applicable laws and the CFPB's mission. It also ensures that supervision decisions are consistent across markets, charters, and regions.

The Office of Enforcement, within SEFL, initiates investigations and enforcement actions, as appropriate, to ensure that providers of consumer financial products and services comply with applicable laws and regulations. Among other duties, CFPB enforcement attorneys manage enforcement cases, provide legal analysis, and support examiners during examinations.

The Office of Fair Lending and Equal Opportunity, also within SEFL, assesses entities' compliance with fair lending laws.

Figure 1 illustrates the SEFL organizational structure.13

Figure 1: SEFL Organizational Structure

Source: OIG compilation based on a review of CFPB documentation.

The CFPB's Integration of Enforcement Attorneys Into Examinations

As noted previously, several federal regulatory agencies have supervision and enforcement authorities over entities that provide consumer financial products and services. These agencies have different approaches for evaluating and enforcing consumer compliance. We learned that many of the CFPB's early hires within the supervision and enforcement functions previously worked at the federal banking agencies or other regulatory agencies. These early hires brought a variety of viewpoints on how the supervision and enforcement functions should work together in executing the agency's supervision and enforcement mandates. CFPB management decided to integrate at least one enforcement attorney into each examination due to perceived benefits of the approach.

According to several CFPB staff, the integrated approach enhances efficiency during the supervisory process. They indicated that integrating an enforcement attorney into each examination from the outset better ensures that if a potential enforcement issue arises, supervision staff do not have to spend substantial time familiarizing the attorney with the facts and circumstances associated with the issue. A senior CFPB official noted that the integrated approach allows the CFPB to compress the fieldwork associated with the examination and any resulting enforcement action into one step.

Guidance Related to the Integration of Enforcement Attorneys Into Examinations

To formalize the integration of enforcement attorneys into examinations, on February 1, 2012, the CFPB issued a one-page policy, Enforcement and Fair Lending Exam Support Activity and the Management of Exam-Generated Legal Issues (examination support policy). This document contains a principles-based description of the agency's expectations for how and when enforcement attorneys should interact with the CFPB's examination teams during various stages of the examination process. Specifically, it describes how the examiner in charge (EIC) shall engage the assigned enforcement attorney during the scoping, fieldwork, and report drafting phases of the examination. According to the CFPB, under this approach, the CFPB's supervision, enforcement, and fair lending functions should collaborate during examinations to realize efficiencies in the supervisory process.

In addition to the examination support policy, the CFPB's examination manual briefly addresses coordination between the agency's supervision and enforcement functions.14 The manual notes that the supervision function will work closely with the Office of Fair Lending and Equal Opportunity and the enforcement function when reviewing fair lending compliance and evaluating other potential violations of federal consumer financial laws. This manual does not supplement or expand on the principles outlined in the examination support policy with regard to the integration of enforcement attorneys into examinations.

Industry Concerns With, and Internal Review of, the Integrated Approach

Some bankers and financial services media outlets have raised concerns about the CFPB's integration of enforcement attorneys into examinations, indicating that the practice can potentially transform examinations into an adversarial process or inhibit communications between the CFPB and supervised institutions. Other industry concerns include the lack of consistent execution of the integrated approach, particularly with respect to the onsite presence of enforcement attorneys at some examinations but not at others. One industry group expressed concern that the CFPB has not provided institutions with an explanation regarding the presence of enforcement attorneys at examinations.

In response to such industry concerns, the CFPB's Ombudsman initiated a review to assess the agency's implementation of the examination support policy. According to the CFPB Ombudsman's Office FY 2012 Annual Report to the Director, as an advocate for a fair process, the Ombudsman met with both internal and external stakeholders to obtain their perspectives on the approach.15 During these sessions, stakeholders shared their understanding of the implementation of the integrated approach. These stakeholders also shared potential benefits of the approach, such as process efficiencies, as well as drawbacks, including the potential for the approach to be a barrier to a free exchange of information during an examination. As a result, the Ombudsman recommended that the CFPB review its implementation of the approach and, in the interim, clarify the role of enforcement attorneys in examinations.

The CFPB subsequently initiated an internal review of the approach. A CFPB official informed us that this effort would evaluate the effectiveness of the integrated approach and determine whether the agency should continue the approach. During our evaluation, we routinely met with senior CFPB officials and shared our preliminary observations concerning the integrated approach, including its potential risks. These meetings occurred while the CFPB's internal review was ongoing.

Completion of OIG Fieldwork and the CFPB's Subsequent Announcement of Plans to Revise the Integrated Approach

In August 2013, we completed the fieldwork phase of our evaluation pursuant to our objectives and scope and initiated the report drafting phase. In October 2013, when our draft report was nearing completion, senior CFPB officials informed us that the agency had finalized its internal review and had reconsidered its approach regarding integrating enforcement attorneys into examinations. CFPB management provided a high-level description of some of the prospective changes to the integrated approach, including its decision to discontinue enforcement attorney participation in onsite examination activities. However, CFPB officials indicated that enforcement attorneys will continue to support examination teams throughout the examination process.

According to CFPB senior officials, the agency's new policies and procedures which reflect its revised approach became effective in November 2013. As these new policies and procedures were issued after we completed the fieldwork phase of our evaluation, we did not review these documents.16

We provided the CFPB an opportunity to provide a response to this report, including any information to address the findings and recommendations of our evaluation. That response is included in its entirety in appendix B.

We intend to conduct follow-up activities to determine whether the actions outlined in the CFPB's response address our findings and recommendations. We will perform these follow-up activities after sufficient time has elapsed to allow us to adequately assess the effectiveness of the agency's response to our recommendations.

- 1. We use the term safeguard to refer to internal controls- the plans, methods, policies, and procedures used to fulfill the mission, strategic plan, goals, and objectives of the organization. Return to text

- 2. Federal consumer financial law, as defined by the Dodd-Frank Wall Street Reform and Consumer Protection Act, includes over a dozen existing federal consumer protection laws, such as the Truth in Lending Act, the Real Estate Settlement Procedures Act, and the Equal Credit Opportunity Act. See Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. No. 111-203, § 1002 (12), 124 Stat. 1376, 1957 (2010) (codified at 12 U.S.C § 5481(12), (14) (2010)). Return to text

- 3. The Federal Reserve Board also supervises other entities, such as bank holding companies. Its supervision authorities include financial holding companies formed under the Gramm-Leach-Bliley Act. Return to text

- 4. Other federal regulatory agencies also have supervision and enforcement authorities relating to consumer financial protection, including the U.S. Department of Housing and Urban Development and the National Credit Union Administration. Return to text

- 5. For further information on the former federal regulatory structure for overseeing consumer compliance matters, see Sean M. Hoskins, A Brief Overview of Actions Taken by the Consumer Financial Protection Bureau (CFPB) in Its First Year, Congressional Research Service, August 29, 2012; David H. Carpenter, The Consumer Financial Protection Bureau (CFPB): A Legal Analysis, Congressional Research Service, June 7, 2012; and David H. Carpenter, The Dodd-Frank Wall Street Reform and Consumer Protection Act: Title X, The Consumer Financial Protection Bureau, Congressional Research Service, July 21, 2010. Return to text

- 6. Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. No. 111-203, § 1011(a), 124 Stat. 1376, 1964 (2010) (codified at 12 U.S.C. § 5491(a) (2010)). Return to text

- 7. The relevant prudential regulator retained primary consumer protection supervisory and enforcement authority for depository institutions with total assets of $10 billion or less. However, the Dodd-Frank Act granted the CFPB the authority to participate in examinations of these smaller depository institutions on a sampling basis. Return to text

- 8. Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. No. 111-203, § 1024(a)(1)(C), 124 Stat. 1376, 1987 (2010) (codified at 12 U.S.C. § 5514(a)(1)(C) (2010)). Return to text

- 9. On July 16, 2013, the Senate confirmed Richard Cordray as the Director of the CFPB. Return to text

- 10. Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. No. 111-203, § 1055(a), 124 Stat. 1376, 2029-30 (2010) (codified at 12 U.S.C. § 5565 (1)(2010)). Return to text

- 11. The CFPB issued these nine public enforcement actions from January 1, 2012, through December 31, 2012. Additional information on these enforcement actions can be found in the CFPB's semiannual report, available at http://files.consumerfinance.gov/f/201303_CFPB_SemiAnnualReport_March2013.pdf. Return to text

- 12. The Consumer Financial Protection Bureau Strategic Plan FY 2013--FY 2017 is available at http://www.consumerfinance.gov/strategic-plan. Return to text

- 13. This organization chart is not comprehensive and includes only detail relevant to this evaluation. Return to text

- 14. The CFPB Supervision and Examination Manual, version 2, was issued in October 2012 and is available at http://www.consumerfinance.gov/guidance/supervision/manual. Return to text

- 15. The CFPB Ombudsman's Office FY 2012 Annual Report to the Director is available at http://files.consumerfinance.gov/f/201211_Ombuds_Office_Annual_Report.pdf. Return to text

- 16. This report describes the policy detailing the CFPB's approach to integrating enforcement attorneys into examinations that was in effect during our fieldwork period, February 2013 to August 2013. As such, we may refer to this policy and the CFPB's associated practices in the present tense throughout this report. We understand that revised policies and procedures reflecting changes to the integrated approach became effective in November 2013. Return to text