IN THIS SECTION

CFPB Report: July 22, 2020

available formats

-

Summary:

HTML -

Full Report:

PDF (2 MB)

The Bureau is funded primarily through transfers from the Board, averaging $487.1 million a year from FY 2012 to FY 2019. We chose to review the Bureau's budget and funding processes.

We determined that the Bureau designed and implemented controls over its budget and funding request processes and the Board designed and implemented controls over the funds transfer process to fulfill the agencies' respective responsibilities outlined in the Dodd-Frank Act. In addition, the Bureau generally complied with legal requirements to produce certain budget- and funding-related information and report it to certain stakeholders.

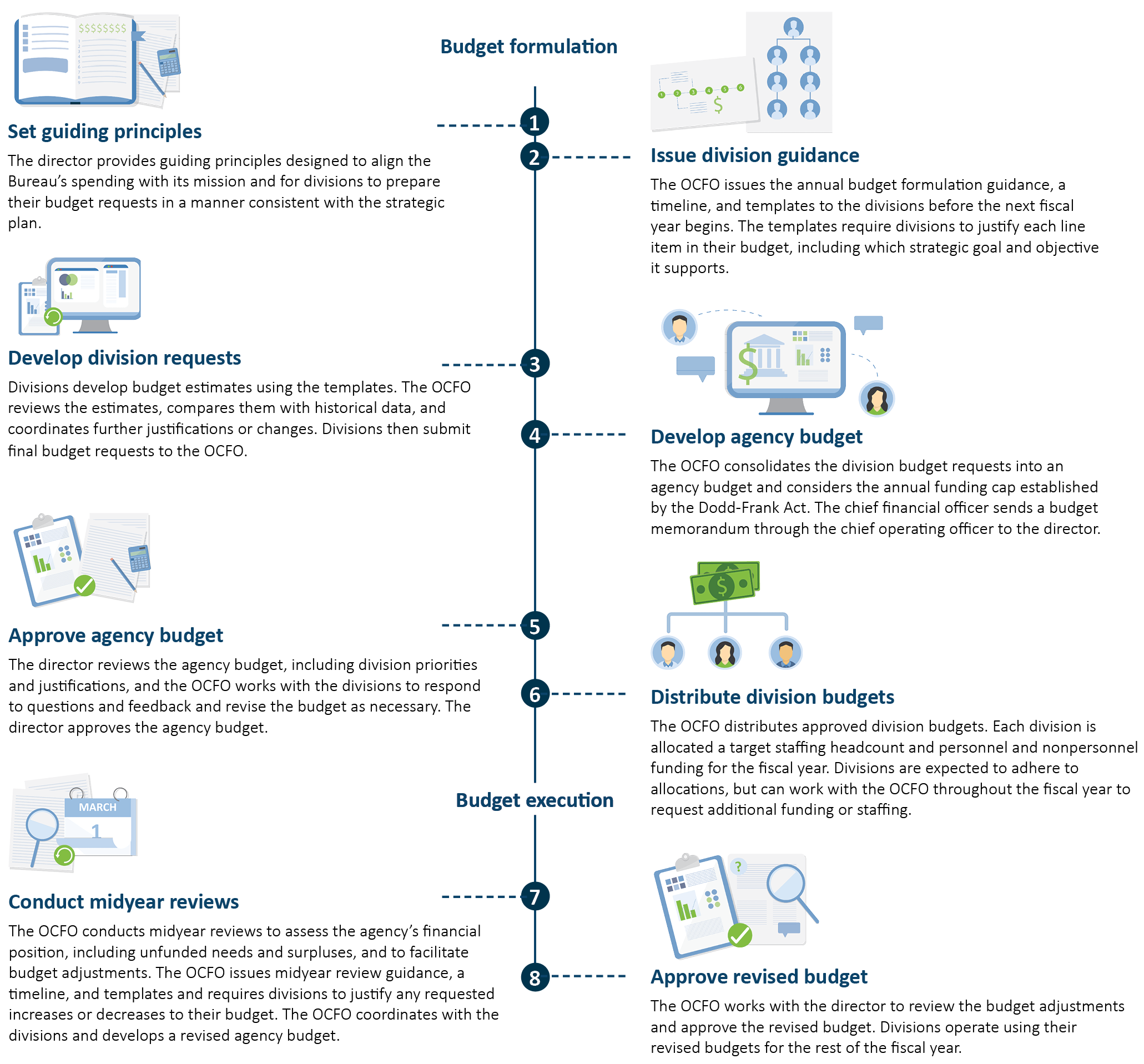

Figure. The Bureau's Budget Formulation and Execution Processes